》View SMM Copper Quotes, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

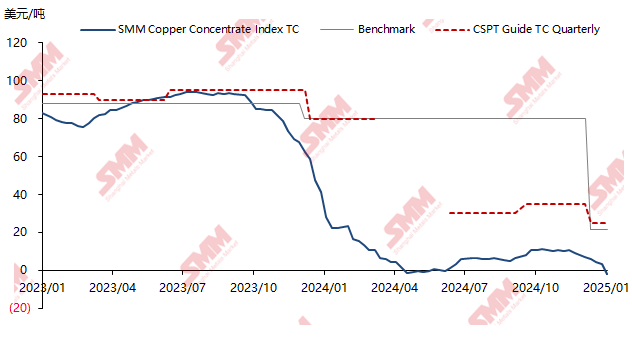

On January 24, 2025, the SMM Imported Copper Concentrate Index (weekly) stood at -$2.2/mt, marking the second time since May 2024 that the TC value turned negative. Unlike previous instances of brief dips below zero, this time the negative TC is likely to persist for a long period.

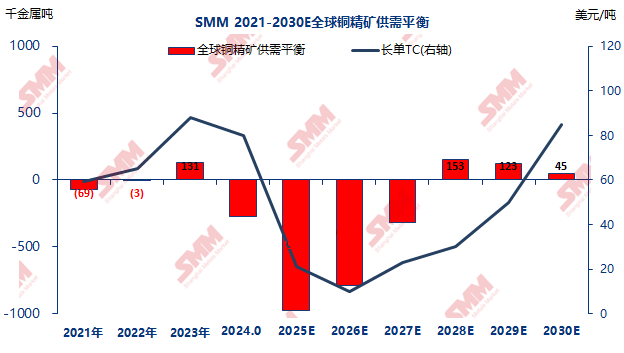

The fundamental cause of the tightness in the spot market lies in the significant expansion of smelters' rough smelting capacity far outpacing the expansion of copper mines. Since 2024, the global supply-demand balance for copper concentrates has been increasingly imbalanced year by year. From 2025 to 2027, there will be a severe gap in the supply-demand balance, with global sulfide ore supply insufficient to meet the demand of smelters' rough smelting capacity.

This imbalance in the supply-demand structure of copper concentrates is reflected in the spot market, where buyers' spot procurement activities have become increasingly active since mid-to-late January 2025. Smelters, in an effort to replenish copper concentrate raw materials for Q1 shipments, have triggered a "price collapse" in the spot market. Moreover, SMM believes this "price collapse" phenomenon will persist for a long time, officially ushering in an era of negative copper concentrate spot TCs.

SMM believes that copper concentrate spot TCs are following the trend of zinc and lead concentrate spot markets, with highly adverse impacts. In my opinion, the main manifestations are as follows: 1. The raw material procurement costs for Chinese copper smelters have risen sharply, potentially leading to escalating losses on production, posing severe challenges to smelters' cash flow and profitability. 2. Malicious competition over raw materials and pricing among Chinese smelters may force some smelters to cut production of finished products, introducing greater operational risks. 3. Such malicious competition among smelters will also severely compress the survival space for copper concentrate traders, with increasingly inverted TCs and prolonged QPs, bringing more operational and financial risks to raw material traders. 4. If Chinese smelters reduce refined production, from a research and market perspective, it will introduce greater uncertainty to future futures market structures, supply-demand balance forecasts, and market prices.

》Click to View the SMM Copper Industry Chain Database